")

Key takeaways

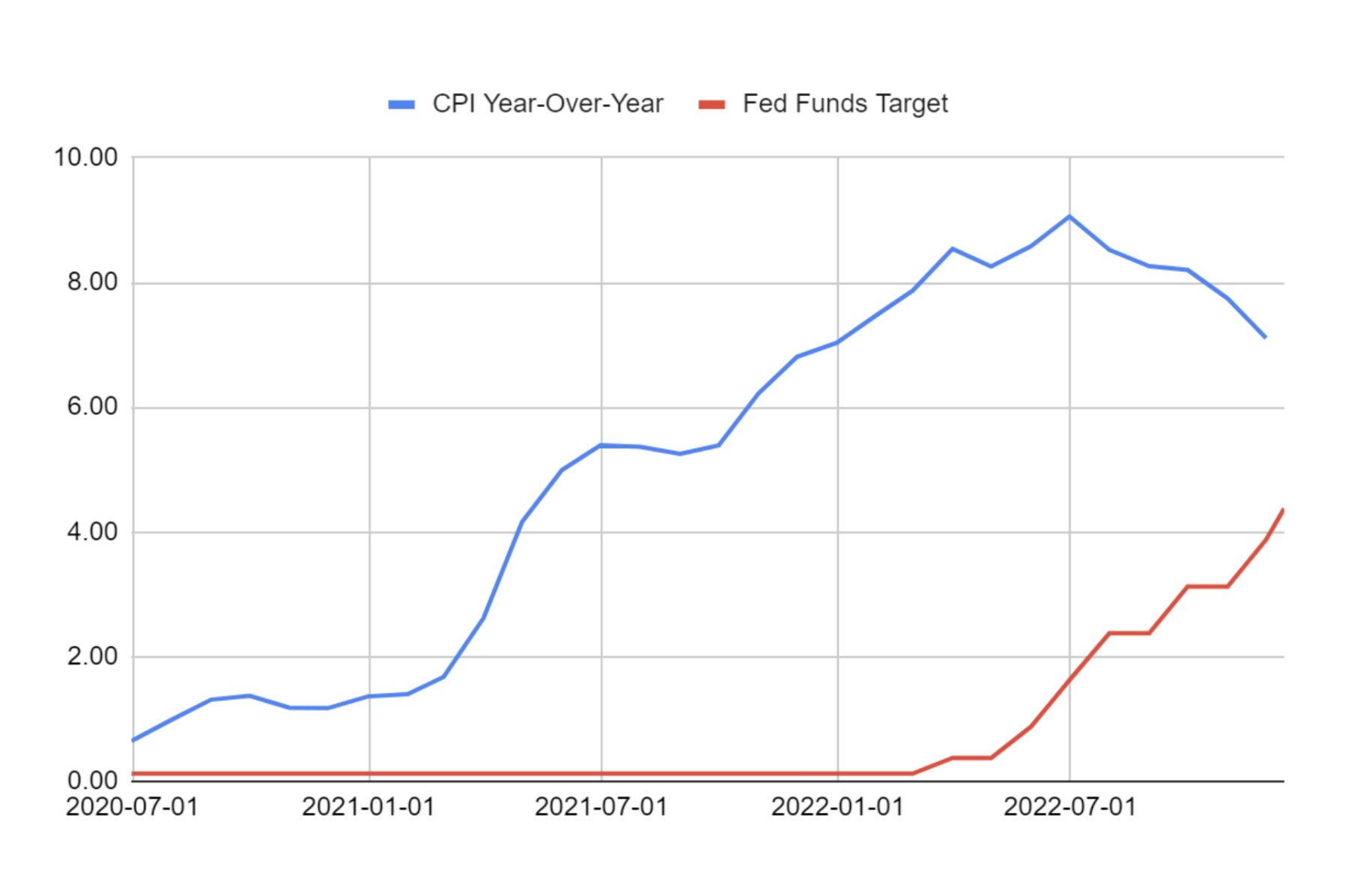

- The Fed increased its target interest rate by 0.5% at this meeting, which is a smaller degree than the prior four meetings, where the Fed hiked by 0.75% each time

- While the Fed has slowed the pace of rate hikes, Federal Reserve Chairman Powell indicated that the Fed has “a ways to go” before they would be done raising interest rates

- Powell said the terminal rate could go higher than expected if inflation does not come down

- The Fed received some good news on the inflation front however, as the latest Consumer Price Index report showed that prices only rose by 0.1% in November

- The Fed’s next meeting isn’t until February 1. Markets are currently split as to whether the Fed will hike by 0.25% or 0.50%. In our view, this question comes primarily down to inflation data

On Wednesday, December 14, the Federal Reserve concluded its last meeting of 2022. It was a historic year for the Fed, which raised its target interest rate by a greater degree than any calendar year in history.

However, this week’s meeting marks a turning point, and likely we’ll look back at this as the beginning of the end of this period of rate hikes. So here are our thoughts on what the Fed said and what it means for you.

What happened: Fed hikes rates but slows the pace

“We understand the hardship that inflation is causing and we are strongly committed to bringing inflation down to our 2% goal.”

The Fed increased its target interest rate by 0.5% at this meeting, which is a smaller degree than the prior four meetings, where the Fed hiked by 0.75% each time. At his post-meeting press conference, Fed Chair Jerome Powell pointed out that general economic growth had slowed, the pace of consumer spending had moderated, and activity in the housing sector had “weakened” significantly. These factors contributed to the Fed’s decision to slow the pace of rate hikes at this meeting.

The Fed has been raising interest rates in an attempt to fight inflation, which this year hit levels not seen since the early 1980s. Powell repeatedly emphasized that the Fed’s resolve to bring inflation down is as strong as ever and that this smaller rate hike does not mean they are satisfied with the level of inflation.

How much longer will the Fed hike rates?

While the Fed has slowed the pace of rate hikes, Federal Reserve Chairman Powell indicated that the Fed has “a ways to go” before they would be done raising interest rates. Several times Powell brought up the “terminal rate,” which is a term for the peak rate the Fed hits during a rate hiking cycle. He said the terminal rate could go higher than expected if inflation does not come down. Several other Fed officials made similar suggestions about the terminal rate in the weeks leading up to this meeting. Whenever you hear several Fed officials repeat the same message, you can bet it is a coordinated communication. This just means that Powell views this as an extremely important point to make.

But what is he really saying? He’s saying that if inflation stays high, the Fed will likely keep hiking for a while, and interest rates could end up materially higher than markets currently assume. This isn’t a very surprising statement. Powell has said repeatedly that the Fed views restoring price stability as job number one. Specifically, at this meeting he said, “Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy.”

Note that this isn’t a promise to hike rates to any given level. Rather it is a promise to keep fighting inflation as long as necessary. So, how long will it be necessary to keep fighting inflation?

Inflation appears to be cooling

The Fed received some good news on that front this week. On Tuesday, the Consumer Price Index report showed that prices only rose by 0.1% in November, 0.2% when excluding food and energy. Both were lower than in October and substantially lower than the pace from earlier in the year.

A look into the details of the report is even more encouraging. The price of goods---essentially any non-food physical item you might buy in a store or online---declined in November. That’s the second month in a row where goods prices have declined.

Perhaps more encouraging is that the CPI, excluding shelter, declined by 0.17% in November. That is notable because the methodology used to estimate inflation in rents and houses is notorious for lagging reality.

In the case of rental units, the Labor Department uses the price of all units in their calculation each month, but since most leases last a year or more, the vast majority of unit prices don’t change. Looking at only new rental agreements, we see that nationwide rent prices are falling slightly.

In November, the category “Rent of Primary Residence” rose by 0.8%, but if current trends continue, that number will fall substantially in the coming months.

The way home prices are reflected in the CPI is even more complicated, but it has a similar built-in lag effect. In November, the official CPI home price figure was +0.7%, which would be about +9% on an annualized basis. We know that home prices aren’t rising at a 9% pace. By most estimates, they are falling modestly.

Eventually, the CPI metric will catch up with reality which, all else being the same, will cause measured inflation to be a lot lower than the current estimate.

What’s next for the Fed?

The Fed’s next meeting isn’t until February 1. Markets are currently split as to whether the Fed will hike by 0.25% or 0.50%. In our view, this question comes primarily down to inflation data. Between now and the February 1 meeting, the Fed will get one more CPI report and two Core PCE inflation reports, the latter being their favored inflation measure. If that fresh data is similar to the November CPI report, we think a 0.25% hike is very likely.

The Fed will be watching other data, especially job growth and consumer spending. However, right now, these data points are important only insofar as they impact inflation. Powell has warned that it will probably take some kind of economic slowdown to bring inflation lower. He repeated this warning at this meeting: “Reducing inflation is likely to require a sustained period of below-trend growth and some softening of labor market conditions.”

But even Powell doesn’t know how much of a slowdown is necessary for inflation to fall. Because of this, expect the Fed to take inflation data at face value. That is to say, if inflation keeps declining, other data points won’t matter. The Fed will be perfectly happy to hike at a slower pace. In fact, there is a good chance that if inflation remains on this downward trend, the Fed could stop hiking altogether after that February 1 meeting.

What does this mean for my portfolio?

For most of 2022, markets were almost exclusively focused on inflation and interest rates. Our view has been that in order for the 2022 bear market to end, two major things needed to happen. The first phase would include some clarity on when inflation would start to subside and, consequently, increased certainty around the Fed’s path of rate hikes. With any luck, this phase is happening right now.

The second phase will be a bit more complicated. The economy has slowed its pace of growth materially and could keep slowing into 2023. Markets will need to ascertain how much this slowdown will impact company profits. The third quarter earnings season didn’t provide much clarity, as many companies warned investors that the coming quarters were highly uncertain.

If markets can get even a small degree of improved clarity about the earnings outlook, that could be enough to form a lasting bull market. Therefore the fourth quarter earnings season, which will kick off in mid-January, will be crucial.

We believe the combination of slower inflation and a less aggressive Fed should be viewed with optimism. The sooner the Fed can stop hiking, the more likely the economy will avoid a deep recession. If there is a mild recession or we manage to avoid a recession altogether, we think it is likely that stocks can continue to rise from here.